Updated: December, 2025

When settling an estate, one of the most consequential decisions is when the home should be sold.

Selling real estate is often a central part of estate settlement — not just a probate issue — and the timing of that sale can affect legal authority, taxes, family dynamics, and how smoothly the estate is resolved.

If you’re looking for a broader overview of the estate settlement process, start with our guide on how to settle an estate.

As a result, people often wonder when a home should be sold:

- Before probate begins?

- During probate while the court is involved?

- Or after probate closes and it becomes an inherited home?

The answer is rarely one-size-fits-all.

In Michigan, the timing of a sale affects legal authority, family dynamics, tax exposure, and out-of-pocket costs in different ways.

Choosing the wrong timing doesn’t usually feel like a mistake right away—but it can create unnecessary delays, stress, or financial consequences later.

This guide is designed to help you understand the tradeoffs between selling:

- before probate

- during probate

- after probate closes

Rather than pushing you toward a single “right” answer, we’ll walk through what typically changes at each stage so you can make a decision that fits the estate’s situation.

A Quick Disclaimer

This article is for educational purposes only and is not legal, tax or financial advice. Selling a home before, during or after probate often involves legal rules, tax considerations, and financial consequences that vary by situation.

Our aim of the article is to reference these different domains at a high-level to help you understand the factors at play and the questions to ask when selling a property — whether inherited or wrapped in probate.

Should You Sell Before Probate

No, probably not. In most cases, a house cannot be sold before probate officially begins and authority has been given.

Until the court appoints a personal representative, the property generally cannot be sold with clear title.

Before probate is opened, no one has legal authority to act on behalf of the estate. Not heirs, not family members, and not even the person named as executor in the will.

There are limited situations where probate may not be required at all, depending on how the home is titled. These scenarios are often confused with “selling before probate,” but they follow different legal rules.

Examples may include:

- Lady-bird deeds or life estates

- Real estate with rights of survivorship

For a clear Michigan-specific explanation of when a home can (and cannot) be sold before probate, see: Can You Sell a House Before Probate in Michigan?

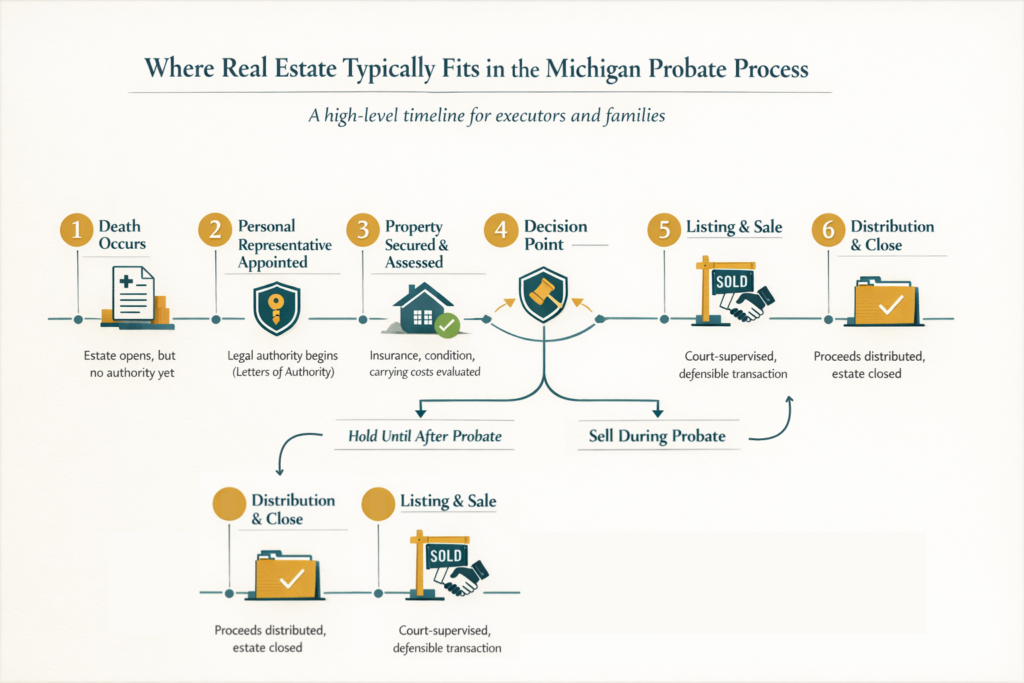

Before we dive too deep, here is a high-level overview of how this real estate decision of when to sell fits into the probate process.

Should You Sell During Probate

Once probate is open, the estate has legal authority to act, but the sale may still be supervised by the court.

For many executors, selling during probate comes down to control, simplicity, and deciding where financial responsibility should live.

This option is commonly chosen when:

- The estate needs liquidity

- Expenses are accumulating

- A mortgage or debt must be paid

- Heirs prefer cash over property

- Simplicity and risk reduction are priorities

Selling during probate is less about market timing and more about orderly, defensible administration. If you want a step-by-step overview of how probate sales work in Michigan, you can review our full guide on selling a home during probate.

Every estate is different, but these are some of the key advantages, disadvantages, and considerations we commonly see when a home is sold during probate.

Pro: Cover Estate Debts & Expenses

Depending on the situation, selling during probate can generate funds to cover ongoing expenses, probate-related fees, and cover any debts owed by the estate.

It is common for many estates to have assets, such as the home, and little cash to cover expenses or debts. In this case, selling the home during probate is a way to prevent the estate from falling behind while administration is ongoing.

Pro: Reduce Costs That Limit Estate Proceeds

Holding onto a property during probate creates holding costs. For some estates, it may simply be utilities and property taxes. For other estates managed by an out-of-state executor, the holding costs may total up to a substantial monthly amount that slowly eats away at the estate proceeds.

We call this the burn rate. Add up all of the monthly ongoing expenses that are related to holding onto the property. This gives you a hard financial number of the cost to hold onto the property.

When compared against the estate’s liquid cash, you get an idea for how long the estate can hold the property. If the amount of time is less than 12 months, the estate may run out of cash before probate closes.

Not figuring out the burn rate is one of the top mistakes executors make that limits estate proceeds.

Pro: Clear (often singular) Fiduciary Authority

Once appointed, the personal representative acts as a fiduciary for the estate. When the executor is a singular person — as opposed to siblings sharing the role — consensus may not be required.

Of course, an executor has a duty to act on behalf of the estate and its beneficiaries, so they cannot do whatever they want.

However, the executor’s function along with court oversight provides a clear legal framework for making decisions about the house rather than relying on familial agreements and consensus.

Selling during probate can help avoid disputes later, particularly situations where all heirs receive title equally and one wants to sell the home and another does not.

By resolving the sale at the estate level, the risk of future partition actions or prolonged disagreements is often reduced.

Pro: Centralized Tax Responsibility

When the home is sold during probate, the transaction and any related tax implications generally remain within the estate rather than shifting to individual heirs or beneficiaries.

Most homes in an estate will not qualify for principal residence exemptions, and therefore, may find themselves subject to capital gains taxes when sold for a profit.

A home sold during probate may result in fewer taxes due to market timing. A decedent’s home will often be valued at fair-market value, or FMV, on the date of death.

When sold close to the date-of-death, it is likely there will be minimal to no capital gains. In addition, there are some rules that the IRS allows when the home is sold within six months of death.

Waiting to sell the property until after probate could create a tax liability for heirs or beneficiaries.

Cons: Court Involvement Adds Time

Probate sales typically require additional steps such as court approval, appraisals, and formal notices. This can make the process slower than a traditional sale and may take several months to complete.

Court-approval is a much bigger deal when the process requires formal probate.

How long probate takes can vary, but the rule of thumb is 8 to 12 months for the average estate in Michigan. With that said, a home listed early in the probate process may not experience any additional time delays.

However, trying to sell a home when the probate process is near the end could add some delays depending on how well the real estate market is doing.

For example, a market where homes sell and close within 60 days is less problematic than a market where homes take 180+ days to close.

Cons: Pricing and Procedural Constraints

In some cases, the court requires the property to be sold within specific parameters (such as a percentage of appraised value), and buyers may face additional uncertainty due to court confirmation requirements.

Selling during probate often makes sense when the priority is reducing risk, settling obligations, and moving the estate forward in a structured way—even if it means accepting additional oversight or a longer timeline.

Sell After Probate

Once probate closes and the estate has finished administration, the home is typically transferred to the heirs.

At that point, the property is no longer governed by probate court oversight, and decisions about selling shift from the estate to the individuals who now own the home.

For some families, this added flexibility is appealing. For others, it introduces new complexity.

This option is commonly considered when:

- The estate has sufficient cash to cover debts and expenses

- Heirs want full control over timing and pricing

- The property will be kept temporarily or improved before selling

- Probate has already been completed or is nearing completion

- A family member is living in the property or tenants exist

The moment probate closes, the questions change. If you’re now dealing with an inherited home rather than an estate asset, our inherited home guide walks through the next phase.

At its core, deciding when to sell a home is not just about probate. It’s about completing the broader estate settlement process.

As with any timing decision, there are benefits and trade-offs to be aware of once the home has been distributed out of the estate.

Pro: No Court Supervision

After probate closes, court approval is no longer required to sell the home and the process is most similar to a standard real estate transaction.

- No probate filings

- No hearings

- No confirmation requirements

In this case, the sale of the home will marry the real estate market and provide a more flexible sales process. It becomes simpler for buyers and sellers alike.

Pro: Greater Control Over Timing & Pricing

Once heirs take ownership, they collectively decide when to sell, how to price the home, and whether to make improvements or repairs.

These kinds of decisions inside probate create unnecessary risk and liability to the executor. Some of the decisions may need court approval, like repairing certain items in the home.

After probate, heirs can choose to wait, renovate, or test the market.

In appreciating markets, this flexibility allows heirs to pursue higher sale prices.

Also, heirs may wish to simply sell as-is and pursue a cash offer from a real estate investor that buys homes.

Con: Disagreements

After probate, title is typically clear and no longer tied to estate administration.

This can reduce procedural friction, but often increases familial and heir friction. Of course, it will depend on how the title was transferred and if any arrangements were made during probate.

However, if a property was inherited with a sibling, consensus may need to be reached. You may find yourself wanting to sell while another family member wants to hold onto the property.

If heirs disagree on timing or pricing, the sale may be delayed or disputes may escalate. In some cases, unresolved disagreements can lead to partition actions or forced sales.

Con: Shift of Tax & Financial Liability to Heirs

Once the home is distributed, ongoing expenses such as taxes, insurance, maintenance, and mortgage payments generally become the heirs’ responsibility.

If multiple heirs are involved, coordination and cost-sharing can become challenging.

If the property is later sold, it may require a “surprise tax bill”.

For example, if the home has capital gains, the liability is based on the heirs and they may be surprised to learn they have a tax liability and coming up with the money could be a challenge.

Be aware everyone is following the possible capital gains requirements.

Tax outcomes depend on timing, basis, and individual circumstances. A CPA can help determine how selling after probate may affect tax liability in your specific case.

Selling after probate can work well when heirs are aligned, finances are stable, and flexibility is the priority. It becomes more challenging when costs are rising, decisions are fragmented, or no clear plan exists.

Con: Disclosure Responsibilities

One important consideration when selling after probate is that disclosure responsibility in Michigan typically shifts from the estate to the heirs.

- During probate, disclosures are often limited because the personal representative may have little to no direct knowledge of the property’s condition.

- After probate closes and the home is transferred, heirs usually sell as individual owners, not as an estate.

Exact requirements for disclosures are laid out in Michigan’s disclosure laws.

When selling after probate, heirs may be required to complete Michigan seller disclosures based on their knowledge, involvement, or possession of the property.

Why this matters:

- Heirs who never lived in the home may feel uncomfortable making representations

- Multiple heirs may have different levels of knowledge

- Disclosure risk becomes personal rather than contained within the estate

Selling after probate can offer more flexibility and control—but it can also increase individual responsibility and potential exposure compared to selling while the property is still held by the estate.

How Most Executors Decide An Option

As you can see, there is a lot to consider on whether to sell a home during or after probate.

Here is a general idea, but your situation may vary:

- When there is cash pressure, risk, or conflict → sell during probate

- When there is alignment, stability, and flexibility → sell after probate

In other words: when protecting the estate matters most, selling during probate is often the safer path. When heirs are aligned and financially stable, waiting until after probate can offer more control.

Final

There is no single “right” time to sell a home connected to an estate.

The best timing depends on legal authority, cash pressure, tax considerations, family dynamics, and where the home sits in the lifecycle—as a probate asset, a newly inherited home, or a property held for years after inheritance.

Because selling decisions can carry legal and tax consequences, it’s important to consult a probate attorney and CPA for guidance specific to your situation.

Our role is to support the real estate decision across the entire estate transition.

We help people sell homes:

- during court-supervised probate

- after probate, once a home becomes an inherited property

- or years later, when an inherited home is finally ready to be sold

Different stages. Different considerations. Same need for clarity.

If you’re unsure which phase you’re in—or what selling option makes sense next—understanding the full lifecycle is often the first step toward a better decision.