Updated: January, 2026

“Why is my Zestimate so low compared to my neighbors,” is a question some homeowners find themselves asking. To answer that question, it helps to understand how homes are valued and how automated-value models work.

If you rely on Zillow’s Zestimate tool for your home’s value, you might feel that the Zestimate is so low. Perhaps you know for a fact that your Zestimate is low because you have a certified, reliable data source such as a home appraisal.

Or, like many, your neighbor’s home just sold significantly more than your Zestimate, and yet, your homes are nearly identical.

Whatever the reason, it’s alarming to see a low Zestimate and even more alarming when you witness a decrease or drop in your Zestimate.

Automated estimates are just one method within a broader home valuation landscape that includes appraisals, market-based analysis, tax assessments, and professional judgment.

Understanding why a Zestimate is low requires understanding where automated value models fit when it comes to home values.

Be cautious when using Zestimate for anything other than general-directional questions. Let’s dive into why your Zestimate is so low. It starts with understanding Zillow’s Zestimate tool.

An Anecdotal Experience With Zestimate

I will dive into the nuts and bolts of the Zestimate…

… but first, an anecdotal story that many experience and a simple way to introduce some of the concepts needed to understand the Zestimate.

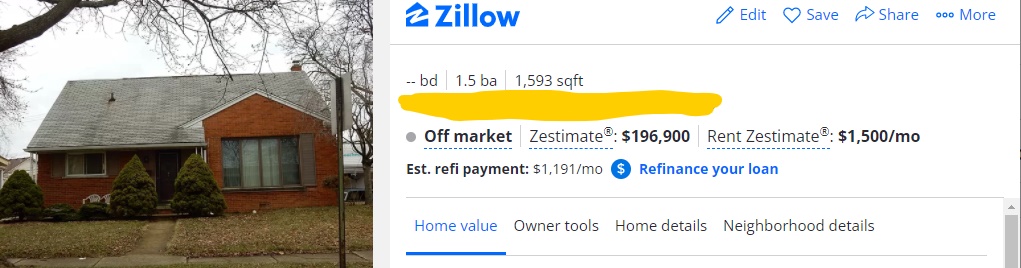

A home in Michigan was purchased in 2021. The property was purchased at the beginning of the wild market-inflation. In particular, the home was part of an estate and was sold shortly after probate.

By all accounts, the home was a fixer-upper.

Based on the appraisal value from the lender, the home’s closing price was 5.5% below market value. After the closing, the Zestimate on the property showed the closing price on the home.

In this case, Zillow assumed the close price was the value of the property.

When we followed up six months after close to monitor the Zestimate, it had only increased about 6% while the rest of the market was growing at 15 to 20%.

By our estimation, the Zestimate was off by more than 25% of the home’s true value.

So why the big discrepancy?

First, Zillow isn’t aware of what the home appraised for. Second, they also are not aware of the updates made to the home following the six-months after purchase.

And that’s the main problem or key to understanding the Zestimate issue.

As the old adage goes, “garbage in. Garbage out.”

How Accurate Is Zillow’s Zestimate

Zillow’s Zestimate has an accuracy of roughly 2% of the final sale price for on-market homes, while off-market homes have a much higher median error rate of roughly 7%.

So, what does this mean?

For off-market homes, 50% of homes have a Zestimate that falls within 7% of the final sale price. For example, a $300,000 sale price would have a Zestimate between $279,000 and $321,000.

Caution With Inference

The median error rate creates confusion and there is temptation to try to apply it individually.

This creates a common but flawed assumption: “If the median error rate is 7%, then my home is probably within 7% of its Zestimate”

That inference does not hold.

Zestimate accuracy works collectively, not individually.

The data may be statistically valid in aggregate, but it cannot be safely worked backward to predict whether any specific property falls near the median — or deep in the tails where errors are much larger.

This is especially important in situations where defensibility matters — estate administration, probate decisions, sibling buyouts, or any context where a value must be justified, documented, and explained. In those cases, a median-based claim of accuracy provides reassurance, not reliability.

Zestimate More Accurate Than Taxable Value and SEV

Even with the limitations, a Zestimate is generally more reliable than taxable value or Michigan state equalized value.

Michigan’s SEV is not designed to measure what a home would sell for. It is an administrative construct, built for taxation, not valuation. Assessors rely on mass-appraisal models, capped growth rules, and statutory constraints that intentionally decouple SEV from real-time market behavior.

By contrast, a Zestimate at least attempts to model market behavior.

Zillow incorporates recent sales, active listings, price trends, and property characteristics in near real time. While the output is imperfect and uneven at the individual level, the inputs are market-oriented, not tax-oriented. That alone makes it directionally closer to value than SEV in most cases.

Put simply:

- SEV is backward-looking and rule-constrained

- Zestimate is forward-looking and market-responsive

That does not make a Zestimate definitive. It makes it less detached.

Failure Point #1: Missing or Wrong Data

When using an automated value model, like the Zestimate, data accuracy plays a critical role. In accurate data causes all sorts of problems with the Zestimate.

One common cause of data inaccuracy is data decay. Gartner reports that every month around 3 percent of data is decayed globally.

While this applies to all data, it’s reasonable to a degree to interpolate and assume that Zillow’s data is decayed by 3% every single month.

Without additional data points being added, like when a home is listed, the more decay that is going to happen. In other words, it’s reasonable to conclude that the longer a home is owned, the more likely the Zestimate is to be wrong.

For example, it’s common for homeowners to:

- Add bathrooms

- Finish a basement

- Add other amenities

- Bump out their garage

Probate and estate-owned homes are especially vulnerable to this problem. These properties are often long-held, infrequently updated, and missing critical data points — sometimes for decades.

Improvements may have been made without permits, room counts may be outdated, condition is rarely current, and deferred maintenance is common.

In many cases, Zillow is effectively valuing a historical snapshot of the property rather than its present reality. This makes automated estimates systematically less reliable for estate properties, where ownership duration, incomplete records, and physical condition diverge most sharply from the data models rely on.

Failure Point #2: Poor Choice in Comparables

Every valuation method depends on selecting appropriate comparable properties. The reliability of any estimated value rises or falls based on how similar those comparables are and how relevant they are to the subject property.

In residential real estate, comparables are typically drawn from nearby homes that have sold within a recent and relevant time window.

While six months is often cited as a general guideline, it is not a fixed rule.

The appropriate time frame can vary based on how stable prices are, how frequently homes sell in the area, and how much property values are changing over time.

Zillow’s Zestimate algorithm tends to apply standardized rules when selecting comparables.

This approach favors consistency, but it also limits flexibility. The algorithm does not meaningfully adjust its comparable selection logic based on local nuance, price movement, or property-specific context.

Timeframe is only part of the issue. The larger limitation is how comparables are prioritized.

Based on observed behavior, Zestimate comparables appear to be selected primarily by proximity, followed by broad size metrics such as square footage.

Other characteristics, such as architectural style, level of renovation, layout efficiency, finish quality, or functional upgrades, carry far less weight than they would in a professional valuation.

This can result in comparisons that look similar on paper but differ materially in real-world value.

Appraisers or experienced real estate professionals typically make conscious tradeoffs when selecting comparables.

A property slightly farther away may be preferred if it more closely matches the subject home’s condition, layout, or improvements. These judgment-based decisions are difficult to replicate in a rigid algorithmic model.

Because automated systems cannot evaluate or prioritize these tradeoffs effectively, they often rely on imperfect substitutes. The result is a set of comparables that are technically similar but functionally mismatched.

When the underlying comparables are poorly chosen, the resulting estimate inherits those weaknesses, regardless of how sophisticated the model appears.

Failure Point #3: No or Poor Adjustments to Comparables

To produce a meaningful valuation, we need apples-to-apples comparisons. That means not only selecting similar homes, but also adjusting for the differences that inevitably remain.

This is where automated models struggle most. When Zillow selects comparables, it generally does not make systematic, property-specific adjustments for differences between the subject property and the homes being compared.

In professional valuation, selecting imperfect comparables is expected, but those imperfections are corrected through adjustments.

Differences in square footage, condition, layout, garage capacity, finishes, or amenities are evaluated and reconciled so the comparison reflects relative value, not just raw sale prices.

Automated estimates do not meaningfully perform this reconciliation.

A comparable that is smaller, less updated, or functionally inferior is typically used at its face sale price, without adjusting upward to reflect those differences. As a result, the estimated value is often pulled toward the lower end of the comparable range.

This is why reviewing the selected comparables matters. If the homes being used are meaningfully different from the property being valued, the estimate is not truly comparable, even if it appears mathematically precise.

Valuation requires more than data selection. It requires judgment to reconcile differences.

Without that step, comparisons drift from apples-to-apples into apples-to-oranges, and the resulting estimate reflects the limitations of the method rather than the value of the property.

Conclusion

A low Zestimate is rarely the result of a single issue. More often, it reflects the cumulative limitations of automated valuation models: incomplete data, imperfect comparables, and the absence of human judgment.

Zestimate can be useful for broad, directional insight, but it is not a substitute for a true home valuation. Valuation is a discipline that blends data, methodology, and judgment, especially when properties are unique, long-held, or tied to estate and probate decisions.

If you’re trying to understand what your home is actually worth, or why different value sources conflict, the right question is not “Why is my Zestimate so low?”

The better question is: Which valuation method fits this property and this decision?