Executive Summary

Purpose

This study evaluates whether the commonly used heuristic that fair market value approximates two times State Equalized Value (2×SEV) can be relied upon for valuation decisions in Michigan probate and estate administration, and whether any defensible correction or alternative heuristic or model can be derived from assessor and taxable value data.

According to the 5,202 Greater Lansing Association of Realtors (GLAR) MLS sales (2025), only 7% of homes sold within ±3% of 2×SEV, while 79% were >±10% off. Taxable value divergence did not predict error. SEV is administratively useful but valuation-unreliable when defensibility, justification and documentation matters.

Background

State Equalized Value (SEV) is a statutory construct created for property taxation, not individualized market valuation.

Nevertheless, the 2×SEV heuristic has become embedded in probate workflows due to its administrative permissibility, convenience, and frequent appearance on inventory forms.

While practitioners generally acknowledge that SEV “may not equal market value,” little empirical evidence has existed to quantify how often the heuristic fails, how large the resulting errors tend to be, or whether assessor-derived data can be used to improve reliability in estate-related contexts.

Methods

Using closed residential sales data from the Greater Lansing Association of Realtors (GLAR) MLS for calendar year 2025, this study analyzed two datasets:

- Estate-related properties (probate, trust, conservatorship listings; n = 180), and

- Total residential market sales (n = 5,202).

Observed market outcomes (net sale price) were compared against the 2×SEV heuristic using a reliability ratio framework. Outcomes were classified into ±3% (reliable), ±10% (ballpark), and ±10% (unreliable) deviation bands.

Exploratory correlation analysis tested whether divergence between SEV and taxable value could predict or bound valuation error.

The results were then compared to automated valuation models for discussion purposes.

Key Findings

- 2×SEV is rarely reliable: Fewer than 9% of estate-related sales and fewer than 7% of total market sales closed within ±3% of 2×SEV.

- When the heuristic fails, it fails materially: Median absolute error was approximately 16.2% for estate-related properties and 19.6% for the total market — translating to typical valuation errors of $40,000 – $55,000 at median price levels.

- No defensible correction exists within assessment data: Divergence between SEV and taxable value explained little to none of the variance in market outcomes (R² ≈ 0.00–0.08). Even in probate-related properties—where long-held ownership and capped values are common — assessment data did not provide a usable predictive signal.

- The heuristic is not merely inaccurate, but non-correctable: Attempts to “adjust” 2×SEV using taxable value behavior are intuitive but empirically unsupported.

Questions Answered From Research

Does SEV equal market value?

No. SEV is a tax assessment construct; it did not reliably match observed market outcomes in this dataset.

Is 2×SEV a reliable estimate of market value?

Usually no. Only 7% of total sales were within ±3% of 2×SEV; 79% were “way off.”

Can taxable value divergence help correct 2×SEV?

No meaningful predictive signal was found (correlation ~0; effectively non-correctable using assessment data alone).

When is SEV “fine” to use?

Low-exposure administrative reporting (e.g., inventory fee calculation) where defensibility requirements are minimal.

What should be used in the middle ground (buyouts / equalization)?

An appraisal-like, documented market analysis — or a certified appraisal when stakes or scrutiny warrant it.

Implications

These findings empirically confirm what many probate practitioners already understand intuitively: SEV is administratively useful, but unreliable for valuation once fiduciary exposure arises.

More importantly, the study demonstrates that no alternative heuristic can be constructed from the same assessment data environment probate permits practitioners to rely upon.

Contribution

This study provides empirical evidence where previously only qualitative caution existed by quantifying the reliability and materiality of the 2×SEV heuristic in Michigan probate contexts.

It demonstrates that assessment-based heuristics not only fail frequently, but cannot be reliably corrected using assessor or taxable value data.

The study further introduces a decision framework that aligns valuation methods with risk, exposure, and defensibility in estate administration.

This study and the published findings is intended as a practitioner reference examining the reliability and defensibility of SEV-based valuation heuristics in Michigan probate and estate administration.

Background & Context

In Michigan, State Equalized Value (SEV) is a statutory construct established under Proposal A of 1994 (see also MCL 211.27a) and is used primarily for property taxation.

By law, SEV is intended to represent approximately 50 percent of a property’s estimated market value, referred to in statute as true cash value.

Although SEV is designed for tax administration, numerical estimates of property value are routinely sought in non-tax contexts, including financial planning, estate planning, and probate administration.

Prior to the widespread availability of automated valuation models, SEV became one such reference point through informal reasoning rather than empirical validation.

From a purely logical standpoint, the inference is straightforward: if SEV represents roughly half of a property’s estimated market value, then doubling SEV should approximate fair market value.

Over time, this reasoning evolved into a commonly cited heuristic, often summarized as “2×SEV equals market value”, used as a quick, back-of-the-envelope estimate by homeowners, real estate professionals, and fiduciaries.

SEV also appears explicitly within probate administration. Under Michigan probate procedure, a personal representative is generally required to file an inventory of estate assets within 90 days of appointment, listing estimated values for real and personal property.

Probate inventory forms permit the use of assessed values, including SEV-based figures, for reporting purposes (See PC 577 Instructions). Because probate filing fees are calculated based on inventory value, modest valuation inaccuracies often result in relatively small fee differences, making SEV-derived estimates administratively convenient.

Beyond inventory reporting, SEV-based figures may also surface informally in estate-related discussions, such as approximate estate value, preliminary asset division or sibling buyouts.

In early or uncontested stages of probate, the presence of SEV within required documentation can create an implicit valuation anchor, even when no formal determination of fair market value has been made.

At the same time, probate and estate administration introduce complexities not present in routine tax assessment.

Valuation decisions may affect tax exposure, fiduciary obligations, inter-family equity, and potential scrutiny from courts or taxing authorities. As a result, property value determinations in probate can carry consequences extending well beyond administrative convenience.

Problem Statement & Research Rationale

The recurring challenge in probate and estate administration is not whether SEV may be used for administrative purposes, but whether SEV-based heuristics can be safely extended into decision contexts where valuation defensibility becomes material.

In response, simplified valuation tools, such as automated valuation models (AVMs) and heuristic rules of thumb, are often relied upon to facilitate decision-making.

Experience in adjacent domains demonstrates that valuation risk arises not from the existence of simplified estimates, but from their use beyond their intended scope.

Automated valuation models, for example, are widely accompanied by disclaimers and limitations, reflecting an industry-wide recognition that reliance, rather than availability, is the primary source of downstream legal and fiduciary exposure.

Between these two extremes lies a substantial gray area: informal probate, family settlements, asset equalization, and sibling buyouts, where cost, convenience, and perceived low exposure often shape valuation decisions.

Decision science and professional practice literature suggest that reliance on heuristics is more likely in environments characterized by infrequent exposure and limited feedback loops.

Prior analysis of Ingham County probate filings indicated that approximately 68 percent of probate matters were handled by attorneys appearing only once during the study period, suggesting that probate administration is episodic rather than continuous for many practitioners.

While this observation does not establish how valuation decisions are made, it provides relevant contextual background: when professionals encounter a process infrequently, reliance on embedded administrative norms and simplified heuristics becomes more likely than in settings with repeated exposure and corrective feedback.

The probate system itself reinforces this dynamic. SEV-derived values appear in required inventory documentation, where modest valuation deviations often have negligible immediate consequences.

The risk emerges when the same heuristic is implicitly carried forward into decisions involving material equity transfers, fiduciary responsibility, or later challenge.

These conditions are further complicated by the rapid expansion of artificial intelligence and automated decision-support tools.

As such systems increasingly assist fiduciaries, attorneys, and beneficiaries in answering valuation-related questions, there is a growing risk that administratively sanctioned heuristics, such as SEV-based rules, may be adopted or amplified without appropriate contextual safeguards.

The existing commentary surrounding SEV-based heuristics generally acknowledges their limitations.

Legal guidance, practitioner commentary, and professional discussions frequently note that assessed values “may not equal market value” and caution against their use in contested valuation settings.

Taken together, these knowledge-based and problem-focused triggers motivated this study.

Research Questions

Primary Research Question

RQ1: Does the commonly assumed heuristic that fair market value approximates two times State Equalized Value (2×SEV) reliably reflect observed residential market outcomes?

Secondary Research Questions

RQ2: When the 2×SEV heuristic fails to approximate market value, what is the typical magnitude of the deviation, and to what extent is that deviation materially significant in estate and probate contexts?

RQ3: How does the magnitude of error associated with the 2×SEV heuristic compare to other commonly relied-upon convenience-oriented valuation methods, such as automated valuation models (e.g., Zestimate), particularly in non-owner-occupied or estate-related properties?

RQ4: If the 2×SEV heuristic proves unreliable, can assessor and taxable value data be used to construct a more defensible proxy for market value within the data constraints typically available to probate practitioners? In other words, does an empirically reliable adjustment or alternative heuristic exist?

Study Objective

By doing so, the study aims to inform decision-making frameworks for estate and probate administration where valuation defensibility, rather than administrative convenience, is the controlling concern.

To our knowledge, no prior empirical analysis has quantified the performance of the 2×SEV heuristic against realized market outcomes at scale, nor evaluated whether assessor-derived adjustments meaningfully improve its reliability in probate-relevant contexts.

Data and Methods

All transaction data were obtained from the Greater Lansing Association of Realtors (GLAR) Multiple Listing Service (MLS) and consist of closed residential property sales occurring between January 1, 2025 and December 31, 2025.

The MLS dataset includes sale price, State Equalized Value (SEV), taxable value, property characteristics, transaction type, and administrative descriptors entered by listing agents.

Residential property was defined for this analysis as single-family residences and condominiums.

Although broader Michigan real estate and lending conventions may classify residential property to include structures containing fewer than four dwelling units, such properties were excluded to reduce structural heterogeneity and because they represent outliers in typical estate and probate contexts. Raw land and commercial properties were excluded.

The MLS was selected because it reflects the same information environment routinely relied upon by real estate professionals, fiduciaries, and probate practitioners when making valuation-related decisions.

Analytical Design

Two complementary analyses were conducted using identical screening and construction criteria unless otherwise noted:

- Estate-Related Properties — a focused subset of properties identified in the MLS as involving probate, trust, or conservatorship contexts.

- Total Market Reliability — a broader analysis of all residential sales to establish baseline heuristic performance.

This dual design allows comparison between estate-relevant conditions and general market behavior, without altering methodological assumptions between samples.

Inclusion and Exclusion Criteria

Geographic Scope

Transactions were included based on agent participation in GLAR, rather than strict county boundaries.

This reflects operational reality in estate administration, where decedents may own property outside their primary county of residence (e.g., seasonal or recreational properties).

Across the final dataset, approximately 88% of transactions occurred within counties commonly associated with the Lansing metropolitan area, including Ingham (52.25%), Eaton (17.61%), Clinton (12.51%), Shiawassee (3.50%), Ionia (1.94%), and Barry (0.46%). Remaining counties are detailed in the Appendix: Figure 1.

Property Type Screening

Raw land and commercial properties were excluded. MLS descriptors and zoning indicators were reviewed to identify residential multi-unit properties (e.g., duplexes); none were identified in the final dataset following screening. This verification did not materially affect either analysis.

New Construction Exclusion

Homes constructed in 2024 or 2025 were excluded to reduce distortion arising from assessor lag, as SEV for new construction frequently reflects land value only rather than completed improvements.

This exclusion was applied uniformly to both analyses but materially affected only the total market dataset.

To validate this cutoff, properties constructed in 2023 were reviewed. Of 21 such properties, three exhibited extreme SEV divergence (SEV values of 19, 21, or indeterminate) and were excluded. The remaining 2023-built properties exhibited SEV-to-market ratios consistent with the broader dataset.

Listings in which SEV was not reported in the MLS (i.e., entered as zero) were excluded, as the absence of SEV data precluded calculation of the reliability ratio.

Analysis 1: Estate-Related Properties

Estate-related properties were identified using MLS descriptors indicating probate, trust, or conservatorship status. Inclusion criteria were:

- Residential property (as defined above)

- Closed between 01/01/2025 and 12/31/2025

- Flagged in the MLS as estate-related

This subset consisted of 180 closed sales.

While MLS descriptors do not provide a legally precise definition of estate status, they represent the best available operational proxy within the MLS environment and align with how practitioners encounter such properties in practice.

Application of the full screening protocol did not materially alter this subset.

Analysis 2: Total Market Reliability

The total market analysis initially included 5,454 closed residential sales occurring within the study period under GLAR jurisdiction.

After applying property type screening and new construction exclusions, the final analytical dataset consisted of 5,202 sales.

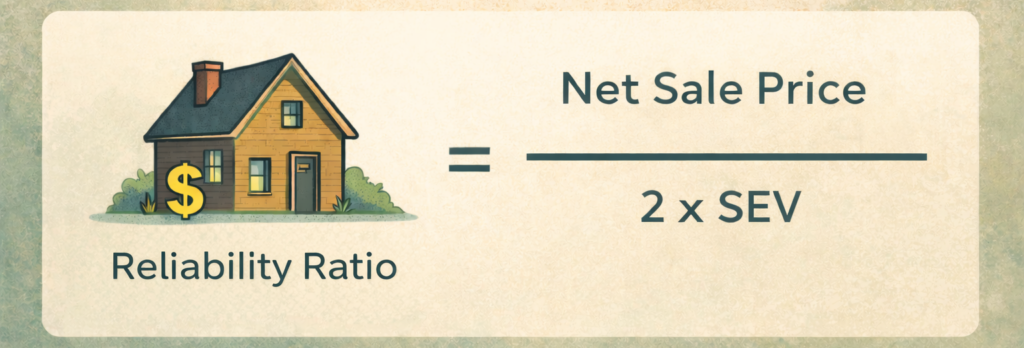

Valuation Metric Construction and Analytical Procedures

Market Value Proxy

For each transaction, net sale price was used as the observed market outcome. Net sale price was calculated as:

Net Sale Price = Closed Sale Price − Seller Concessions

Reliability Ratio

To evaluate the performance of the 2×SEV heuristic, a reliability ratio was constructed for each property as follows:

Reliability Ratio = Net Sale Price / 2 × SEV

A reliability ratio of 1.00 indicates exact alignment with the 2×SEV heuristic. Values above or below 1.00 indicate deviation from the heuristic in either direction.

This ratio-based approach was selected to:

- normalize valuation differences across price ranges, and

- directly test the commonly assumed equivalence between fair market value and 2×SEV.

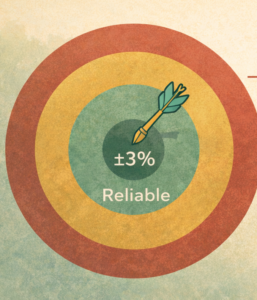

Reliability Band Classification

Reliability ratios were grouped into predefined deviation bands to distinguish outcomes where reliance on the heuristic could reasonably be described as reliable versus unreliable in fiduciary contexts. The following bands were applied:

- ±3% — Reliable

- ±10% — Ballpark (directional, not defensible)

- >±10% — Unreliable

Band classifications were implemented using pivot tables to quantify the proportion of transactions falling within each range.

Justification for the ±3% band is found in the discussion section through various frames of reference.

Correlation Analysis

To test whether assessor-derived data could provide predictive signal for the reliability of the 2×SEV heuristic, correlation analysis was conducted using absolute dollar divergence measures.

Specifically, the analysis evaluated the relationship between:

- SEV – Taxable Value (in dollars), representing the magnitude of divergence between assessed value and capped taxable value, and

- Deviation from the 2×SEV heuristic, measured as the absolute dollar difference between net sale price and 2×SEV.

Dollar-based measures were intentionally selected to avoid distortions that can arise when correlating ratios with shared denominators.

Using absolute dollar divergence ensures that the analysis reflects material valuation differences, rather than proportional artifacts driven by scale effects or small denominators.

Pearson correlation coefficients and coefficients of determination (R²) were calculated to assess whether greater divergence between taxable value and SEV was associated with larger deviations from the 2×SEV heuristic.

Distributional and Quartile Analysis

To evaluate the magnitude of deviation when the heuristic failed, reliability ratios were sorted into quartiles.

Median deviation within each quartile was calculated and then applied to the median sale price of the dataset to estimate the corresponding dollar magnitude of valuation error.

Absolute values of median deviation were used when computing error magnitude to enable comparison with published median absolute error statistics reported by automated valuation models.

This approach allows deviation to be expressed not only as a percentage, but as a material dollar impact relevant to estate and probate decision-making.

Comparative Error Framing

Median absolute deviation from the 2×SEV heuristic was calculated for:

- the full market dataset, and

- the estate-related subset.

These values were used to provide contextual comparison with publicly reported AVM accuracy metrics, recognizing differences in methodology and disclosure practices.

Findings

Dataset 1: Estate-Related MLS Listings

A focused subset of 180 closed sales was extracted from the GLAR MLS for 01/01/2025–12/31/2025, consisting of listings identified by MLS descriptors indicating probate, trust, or conservatorship context.

This subset is intended to approximate the type of residential property most commonly encountered in estate administration workflows, recognizing that MLS labeling is an operational proxy rather than a legal classification.

Reliability Bands For Estates

The reliability bands measured how often 2×SEV matched market outcomes.

Using the study’s reliability ratio (net sale price ÷ 2×SEV), sales were classified into three performance bands:

- Reliable (±3% of 2×SEV): 8.89%

- Ballpark (±10% of 2×SEV): 15.00%

- Unreliable (>±10% from 2×SEV): 76.11%

In this estate-related dataset, fewer than 1 in 10 sales closed within a ±3% band around 2×SEV, while roughly 3 in 4 sales were more than 10% away from 2×SEV.

Central Tendency: Typical Error

To compare against AVM-style reporting (which often uses a median error framing), the median absolute percent error of the 2×SEV heuristic in this dataset was:

Median error: 16.20%

Even before looking at “worst cases,” the typical estate-related sale deviated from 2×SEV by about 16% — a level of error that is meaningful in most fiduciary contexts because it can directly affect equity distributions, buyouts, and defensibility.

Magnitude of Error When the Heuristic Fails

Because fiduciary risk is driven not only by how often a heuristic misses, but how far it misses, the distribution of error was summarized using quartiles.

Using the dataset’s median sale price ($238,450) as a material reference point, the quartiles of deviation (absolute) were:

| Quartile | Deviation Level | Approx. Dollar Impact at Median Sale |

|---|---|---|

| Q1 | 10.22% | $24,364.90 |

| Q2 (Median) | 18.36% | $43,773.43 |

| Q3 | 34.71% | $82,767.82 |

When 2×SEV is wrong in estate-related listings, it is often not “a little wrong.”

Even at the lower quartile, the implied variance is five figures. At the median and upper quartiles, the implied variance rises into mid-five figures to low-six figures, which is exactly where beneficiary disputes, buyout inequities, and hindsight scrutiny tend to cluster.

Can Taxable-to-SEV Divergence Predict When 2×SEV Will Be “Close”?

A common assumption in practice is: “If taxable value is far below SEV (capped/long-held), then SEV is probably disconnected from market—so we can ‘adjust down’ from 2×SEV and be safe.”

To test whether that intuition produces a usable signal, we examined the relationship between:

- X: dollar divergence between SEV and taxable value (SEV − taxable value), and

- Y: the heuristic’s reliability ratio (net sale price ÷ 2×SEV), expressed as deviation.

In the estate-related dataset, the relationship was weak:

- Correlation (r): −0.28

- R²: ~0.08

Taxable-to-SEV divergence explains only about 8% of the variation in how far sale outcomes deviate from 2×SEV.

Practical Interpretation for Estate Contexts

In practical terms, these findings indicate that:

- 2×SEV is rarely accurate for estate-related properties.

- When inaccurate, the resulting valuation error is frequently large enough to affect beneficiary equity, settlement negotiations, and fiduciary exposure.

- Common attempts to “correct” the heuristic using assessor-derived data do not reliably reduce error.

Put plainly: In approximately four out of five estate-related cases, reliance on the 2×SEV heuristic would have produced a materially misleading estimate of market value.

While Dataset 1 reflects properties most likely to resemble inherited or fiduciary-managed homes, the next analysis examines whether these patterns persist across the broader residential market.

Dataset 2: Total Market

Dataset 2 consists of 5,202 closed residential sales recorded in the Greater Lansing Association of Realtors (GLAR) MLS between January 1, 2025 and December 31, 2025, following application of the same screening and exclusion criteria used in Dataset 1.

Properties identified as raw land, commercial, or new construction (2024–2025 builds) were excluded to reduce distortion arising from assessor lag and non-representative valuation dynamics.

This dataset represents the broader residential market encountered by homeowners, real estate professionals, and fiduciaries, and serves as a baseline against which estate-related performance can be evaluated.

Reliability Bands In Total Market

Using the same reliability ratio and deviation bands applied in Dataset 1, sale outcomes in the total market dataset were classified as follows:

- Reliable (±3%): 6.71%

- Ballpark: (±10%): 15.63%

- Unreliable (>±10%): 77.66%

In summary, fewer than 1 in 15 residential sales closed within ±3% of the 2×SEV heuristic and ,ore than three-quarters of transactions deviated by more than ±10%.

Even under a broad ±10% tolerance, nearly 80% of sales remained materially misaligned with the heuristic.

These results indicate that the limited reliability observed in estate-related properties is not unique to fiduciary contexts, but reflects broader market behavior.

Central Tendency: Typical Error Compared to Alternative “Convenience” Models

To facilitate comparison with commonly reported automated valuation model (AVM) metrics, median absolute error was calculated for the total market dataset.

Median absolute error relative to 2×SEV: 19.59%

At the dataset’s median sale price of approximately $239,450, this corresponds to a typical valuation deviation of roughly $47,000.

Magnitude of Error When the Heuristic Fails (Quartile Analysis)

To assess how far the heuristic deviates when it fails, absolute deviation from 2×SEV was summarized using quartiles and applied to the median sale price.

| Quartile | Deviation Level | Approx. Dollar Impact |

|---|---|---|

| Q1 | 11.19% | $26,785.81 |

| Q2 (Median) | 22.78% | $54,543.54 |

| Q3 | 38.76% | $92,804.18 |

When the heuristic fails in the general market, the resulting valuation error frequently reaches mid-five figures, with upper-quartile deviations approaching six figures.

These outcomes are not isolated outliers but represent central tendencies within the distribution.

Can Taxable-to-SEV Divergence Predict When 2×SEV Will Be “Close”?

As in Dataset 1, correlation analysis was conducted to test whether divergence between SEV and taxable value (measured in dollars) provides a usable signal for predicting deviation from the 2×SEV heuristic.

In the total market dataset, the relationship between SEV–taxable divergence and deviation from 2×SEV was effectively zero, with negligible explanatory power.

The assumption that capped or long-held properties can be reliably adjusted from 2×SEV using assessor data is not supported by the data.

No stable or correctable relationship exists within assessor-derived inputs that materially improves heuristic accuracy in the general residential market.

Comparative Interpretation: Estate vs. Total Market

Comparing Dataset 1 and Dataset 2 yields two important insights:

- Estate-related properties performed only marginally better than the total market (median error ~16% vs. ~20%), but still far outside reliable bounds.

- The general residential market does not rescue the heuristic; if anything, it confirms that poor reliability is systemic rather than situational.

Put simply: The 2×SEV heuristic is unreliable both where fiduciary risk is highest (estate-related properties) and where market data is most abundant (the general residential market).

Having established that the 2×SEV heuristic performs poorly across both estate-specific and general market conditions, and that no corrective signal exists within assessor-derived data, the next section examines what this means for valuation defensibility and decision-making in probate and estate administration.

Discussion

Why the 2×SEV Heuristic Fails

The findings demonstrate that the commonly assumed 2×SEV heuristic aligns closely with observed market outcomes in only a narrow minority of residential sales.

More importantly, deviations outside that narrow range are not trivial statistical noise, but materially significant in the contexts where estate and probate valuation decisions carry fiduciary and legal consequences.

This failure is structural rather than incidental.

State Equalized Value is produced through mass assessment processes designed for tax administration, not individualized market valuation.

The data show no evidence that the heuristic’s errors are bounded, predictable, or directionally consistent.

As a result, reliance on 2×SEV beyond narrow administrative contexts exposes fiduciaries to valuation variance that cannot be anticipated or mitigated using assessment-based information alone.

Materiality and Fiduciary Impact: Why “Close Enough” Is Not Defensible

Materiality in estate administration must be evaluated in real-world terms rather than abstract percentages.

At median residential price levels in the Greater Lansing market, a ±3 percent deviation from 2×SEV represents approximately $7,200–$7,500.

While this amount may appear modest in isolation, it represents more than 10 percent of Michigan’s median household annual income, or roughly one month of earnings.

For beneficiaries, valuation error is experienced as concentrated harm rather than diversified risk. In many estates, the primary residence constitutes the dominant asset, and valuation variance directly alters distributive equity.

A $7,500–$25,000 deviation can meaningfully affect beneficiary outcomes and often becomes the focal point of dispute.

This proportional impact is magnified in retirement-age and fixed-income households, where home equity represents a substantial share of net worth. In such cases, valuation variance of several thousand dollars may equal months of discretionary income, annual property tax obligations, or funds reserved for healthcare and living expenses.

Materiality is also appropriately framed relative to probate administration costs. In Michigan, the total cost of informal probate commonly falls within the same range as the valuation error produced by modest heuristic deviation.

This creates a paradox: reliance on a shortcut intended to save cost may introduce an error equal to—or greater than—the cost of employing a more defensible valuation method at the outset.

Permissibility Versus Reliability

A central distinction emerging from this analysis is the difference between legal permissibility and empirical reliability.

Michigan probate procedures permit the use of SEV-based figures for inventory and administrative reporting, reflecting efficiency and standardization needs.

Permissibility establishes what may be used; reliability determines when reliance is justified.

Courts, beneficiaries, and taxing authorities evaluate valuation decisions retrospectively, with attention to whether the method used was reasonable given the exposure involved and the availability of more defensible alternatives.

A ±10 percent deviation — representing $20,000–$25,000 at median prices — may be acceptable for preliminary orientation or informal discussion.

It is far more difficult to defend when valuation decisions affect asset division, buyouts, or tax reporting. In fiduciary contexts, approximate usefulness and defensible reliability are not equivalent.

The Failure of Intuitive Adjustment and Heuristic Refinement

A common informal practice in probate valuation is to begin with 2×SEV and apply discretionary adjustments based on perceived property condition or assessment lag.

Properties with material divergence between taxable value and SEV are often assumed to be more likely to deviate from market value and therefore “adjusted downward.”

The data do not support this intuition. Exploratory analysis demonstrated no meaningful relationship between divergence in taxable value and deviation from the 2×SEV heuristic.

This result is significant not because it reveals bias, but because it confirms indeterminacy. Even legally meaningful variables embedded in Michigan’s tax framework do not provide a usable signal for bounding valuation risk.

Automated Valuation Models, Convenience Demand, and the Limits of Rule-Based Valuation

The findings of this analysis are further contextualized by comparison to automated valuation models (AVMs), such as Zillow’s Zestimate.

Even AVMs that report median error rates below 10 percent explicitly caution against fiduciary reliance, disclose known limitations, and acknowledge heightened error for off-market, infrequently transacted, or condition-variable properties.

These disclosures reflect an industry-wide recognition that valuation risk arises not merely from error, but from reliance in contexts where defensibility matters.

In contrast, the median error associated with the 2×SEV heuristic observed in this analysis materially exceeds commonly disclosed AVM benchmarks.

If valuation systems with lower median error still require prominent disclaimers and usage limitations, reliance on a heuristic with higher and unbounded error cannot reasonably be treated as defensible in fiduciary settings.

The issue is not whether the heuristic is occasionally close, but whether its error can be anticipated, bounded, or justified after the fact. The evidence suggests it cannot.

At the same time, this comparison highlights a broader and persistent systemic condition: the demand for convenient, low-cost valuation tools in gray-area decisions where formal appraisal feels disproportionate. That demand is rational.

These dynamics are increasingly relevant as artificial intelligence and automated decision-support tools become embedded in legal, financial, and fiduciary workflows.

Simplified rules, automated value models and heuristics — particularly those already institutionalized through administrative processes — can appear authoritative while performing unreliably when extended beyond their intended scope.

Without explicit attention to exposure, materiality, and defensibility, AI systems risk replicating and scaling heuristic misuse rather than correcting it.

Where valuation outcomes carry fiduciary, legal, or tax consequences, the appropriate response is not to search for a better shortcut, but to align the valuation method with the level of risk and defensibility required.

Summary Interpretation

The findings of this analysis empirically confirm what many probate practitioners already understand intuitively: State Equalized Value is administratively useful, but unreliable as a proxy for fair market value once fiduciary exposure arises.

At the same time, practitioners also recognize that certified appraisals represent the highest standard of defensibility in contested, taxable, or litigated matters.

In these “middle ground” scenarios, reliance on SEV-based heuristics introduces risk, yet the cost and formality of a certified appraisal may feel disproportionate.

This creates a structural gap in valuation practice: SEV is too weak, appraisal may be excessive, and no assessment-based heuristic can safely fill the space between them.

The findings of this study demonstrate that this gap cannot be resolved through refinement of the 2×SEV heuristic or adjustment based on taxable value behavior.

Empirically, no correction function exists within the assessment data environment that reliably predicts when SEV-based estimates will approximate market outcomes. As a result, attempts to “adjust” SEV in the middle ground rely on intuition rather than evidence.

What distinguishes defensible valuation in these scenarios is not the elimination of judgment, but the quality and documentation of judgment.

Once valuation decisions move beyond purely administrative reporting, defensibility requires a method that incorporates observable market evidence, property-specific analysis, and accountable professional reasoning without necessarily invoking the full procedural weight of a certified appraisal.

The following framework is intended to address that question.

Decision Framework: Risk, Exposure, Justification, and Method

The findings of this study narrow the valuation problem faced by probate and estate practitioners to a practical question of proportionality.

It is well understood that State Equalized Value (SEV) is administratively useful but unreliable for valuation, and that certified appraisals represent the highest standard of defensibility in contested or high-exposure matters. The unresolved issue lies between these two endpoints.

That issue is not whether a middle ground exists, but what qualifies as a defensible middle ground.

This framework approaches valuation selection as a decision-theoretic problem governed by four interrelated factors:

- Risk: the likelihood the valuation will be questioned or reviewed

- Exposure: the financial, fiduciary, relational, or tax consequences of error

- Justification: the level of explanation and documentation required after the fact

- Method: the valuation approach capable of meeting the required level of justification

As risk and exposure increase, the burden of justification increases accordingly. When that burden exceeds what heuristics or automated outputs can provide, valuation methods must evolve toward approaches that resemble formal appraisal reasoning — even if a full appraisal is not yet required.

Are Real Estate Agents a Suitable Middle Ground?

Once heuristics fail, the relevant question is not whether a valuation method is informal or formal, but whether it performs the functional role of an appraisal at a proportional level.

Certified appraisals are not uniquely defensible because of licensing alone, but because they apply a disciplined methodology:

- systematic selection of comparable sales

- reasoned adjustments based on condition, location, and market forces

- documented assumptions and conclusions

- accountability to professional standards

Any middle-ground valuation method must approximate these functions to be defensible.

This distinction is critical when considering the role of real estate agents. While agents are often treated as interchangeable sources of opinion, the data environment and professional reality suggest otherwise.

However, some agents—by virtue of experience, transaction volume, training, and pricing methodology—operate much closer to appraisal logic than to heuristic estimation.

Operational Application: Selecting Valuation Methods by Exposure Level

Valuation method selection in probate and estate administration should be driven by the nature of the decision being made, not by habit, convenience, or the mere availability of a number.

The appropriate method depends on the level of exposure created by the decision and the degree of justification that may be required later.

Rather than asking “What value should we use?”, fiduciaries should ask “What is this value being used for?”

Low Exposure: Administrative and Procedural Contexts

Typical decisions

- “What is the approximate value of the estate for inventory purposes?”

- “What value is required to complete procedural filings?”

- “What number is needed to calculate administrative fees?”

Risk & Exposure:

- Low

- Valuation has no direct distributive or adversarial effect

Justification Required:

- Minimal

- Consistency and permissibility are sufficient

Appropriate Method: SEV-based figures or other administratively permitted proxies

In this context, valuation serves a procedural function, not a decision function. Precision does not materially change outcomes, and the cost of higher defensibility would exceed the benefit.

Moderate Exposure: The Gray Area Where Method Matters Most

Typical decisions

- “How much money should change hands between siblings?”

- “How should assets be equalized across beneficiaries?”

- “What value should be used for fiduciary accounting or negotiated settlement?”

- “Is this valuation fair if reviewed later?”

Risk & Exposure

- Moderate but real

- Decisions materially affect beneficiary outcomes and may be scrutinized retrospectively

Justification Required

- Substantive

- Valuation must be explainable, reconstructible, and grounded in market evidence

Assessment-based heuristics fail at this level. No adjustment using taxable value or assessor data reliably predicts or bounds error. The valuation method must function like an appraisal, even if a formal appraisal is not yet required.

At this level, method matters more than labels. The defensibility of the valuation depends on whether the reasoning can be evaluated and defended after the fact. Not on whether it carries a particular title. An agent may be appropriate, but an appraiser may be needed.

High Exposure: Formal Scrutiny and Adversarial Contexts

Typical decisions

- “What value will be reported to the IRS?”

- “What value will be presented in court?”

- “What valuation must withstand challenge by adverse parties?”

Risk & Exposure

- High

- Valuation is likely to be contested or formally reviewed

Justification Required

- Maximum

- Independent, standardized, and professionally regulated

Appropriate Method: Certified appraisal performed by a licensed appraiser in accordance with professional standards

At this level, proportionality favors formality. The cost and rigor of appraisal are justified by the consequences of error.

| Decision Context | Example Question Being Answered | Exposure Level | Justification Required | Appropriate Method |

|---|---|---|---|---|

| Administrative | “How much is the estate worth for inventory?” | Low | Minimal | SEV / administrative proxy |

| Distributive / Negotiated | “How much money should change hands between siblings?” | Moderate | Substantive | Market-based, appraisal-like analysis |

| Adversarial / Tax | “What value must withstand IRS or court review?” | High | Maximum | Certified appraisal |

Diagnostic Questions for Practitioners

Proposed questions before choosing a valuation method

To identify low exposure

- Is this value used only for procedural filing?

- Would a 10–20% variance materially change anyone’s outcome?

- Is this number unlikely to be relied upon later?

If yes → administrative proxy is likely sufficient.

To identify moderate exposure (middle ground)

- Will money change hands between beneficiaries?

- Could this valuation be questioned months or years later?

- Would a beneficiary reasonably argue the value was unfair?

- Would I be comfortable explaining this valuation in writing after the fact?

If yes → heuristic methods are insufficient; appraisal-like reasoning is required.

To identify high exposure

- Is this value being reported to the IRS or court?

- Is litigation, objection, or audit foreseeable?

- Would this valuation need to stand on its own under formal scrutiny?

If yes → certified appraisal is required.

<h3>Core Insight (Reframed)</h3>

The central insight of this framework is not that one valuation method is universally superior, but that valuation methods must scale with exposure.

- SEV works where valuation is administrative.

- Heuristics fail where valuation affects outcomes.

- Appraisal-like analysis governs the middle ground.

- Certified appraisal anchors high-risk decisions.

Valuation risk cannot be managed by convenience alone. Where exposure exists, defensibility must be intentional — and that begins by asking the right question before selecting a method.

Limitations and Ethical Boundaries

The purpose of this section is to clarify the scope of the analysis and to distinguish decision support from professional or legal judgment.

This paper is not intended to provide legal advice, tax advice, or appraisal services. Nothing herein should be construed as a substitute for independent legal counsel, certified appraisal, or other professional determinations required under law or regulation.

Rather, this analysis is intended to support method selection decisions by highlighting the limits of heuristic valuation approaches under varying levels of risk and exposure.

Analytical Scope and Data Constraints

This study does not assert that no improved valuation heuristic exists under any circumstances. Instead, it demonstrates that no empirically reliable corrective heuristic can be derived from the assessor and taxable value data commonly available and relied upon in probate and estate administration.

A key limitation of this analysis is that it evaluates heuristic reliability solely within the informational environment typically accessible to probate practitioners — namely assessed values, taxable values, and observable transaction outcomes.

While it is theoretically possible that more accurate or condition-sensitive heuristics could be developed using richer inputs (such as interior condition assessments, renovation history, deferred maintenance, functional obsolescence, or fine-grained neighborhood segmentation), such variables are not systematically captured in assessor records nor readily available within standard probate workflows.

As a result, any heuristic constructed from legally permissible tax and assessment data must operate under significant informational constraints. This analysis demonstrates that within those constraints, no stable or correctable relationship exists that meaningfully improves upon the commonly used 2×SEV heuristic.

Ethical Use of Findings

The conclusions of this study should not be used to justify informal valuation practices in high-exposure contexts, nor to displace professional appraisal where defensibility is required.

The findings instead reinforce the importance of aligning valuation methods with fiduciary risk, legal exposure, and justification requirements.

Analytical design, data interpretation, and conclusions are the author’s own. Drafting and structural assistance tools were used to support clarity and organization.

Conclusion

Valuation in probate and estate administration is not fundamentally a question of numerical accuracy. It is a question of defensibility proportional to risk.

This study demonstrates that the commonly relied-upon 2×SEV heuristic performs poorly across both estate-related properties and the broader residential market.

More critically, it shows that the heuristic’s errors are not small, predictable, or correctable using assessor-derived data. When the heuristic fails, it often fails by amounts large enough to affect beneficiary equity, trigger disputes, and expose fiduciaries to hindsight scrutiny.

These findings empirically confirm what many practitioners already know intuitively: State Equalized Value is suitable for administrative convenience, but unreliable as a stand-in for fair market value once decisions carry material consequences.

The study advances that intuition by quantifying how often the heuristic fails, how large the errors tend to be, and by demonstrating that no defensible adjustment function exists within the tax assessment data environment.

Importantly, the failure of the 2×SEV heuristic does not imply that every estate decision requires a certified appraisal. Nor does it suggest that automated valuation models should replace SEV in fiduciary contexts.

Rather, it clarifies that once valuation decisions affect outcomes, heuristics and automated outputs cease to be sufficient—not because they are imperfect, but because they are not defensible after the fact.

The central challenge in probate practice lies in the middle ground: decisions that are more consequential than administrative reporting, yet do not rise immediately to formal litigation, court proceedings, or tax adjudication.

In this space, the findings show that convenience-based valuation cannot be made safe through refinement. Instead, defensibility must be achieved through method selection, not better shortcuts.

The framework proposed in this paper addresses that gap. It reframes valuation choice as a function of exposure, justification, and accountability, rather than habit or availability. Where exposure is low, SEV remains appropriate. Where exposure is high, certified appraisal is required.

Between those points, valuation must evolve toward appraisal-like reasoning—grounded in observable market evidence, transparent logic, and professional accountability—even if a full appraisal is not yet warranted.

Ultimately, valuation risk cannot be managed by convenience alone. Where exposure exists, defensibility must be intentional. That begins not by asking “What number can we use?”, but by asking “What decision is this value being used to support—and how defensible must that decision be later?”

That distinction, more than any specific metric, defines responsible valuation practice in probate and estate administration.

Appendix

Key definitions (Michigan):

- SEV: State Equalized Value; intended to be ~50% of true cash value for assessment.

- Taxable Value: the lesser of SEV or capped value (Proposal A mechanics).

- True Cash Value / Estimated Market Value (assessment context): assessor’s estimate for taxation.

- Fair Market Value (FMV): willing buyer/willing seller standard (valuation context).

- 2×SEV heuristic: an inference people use; not a statutory valuation method.

Frequently Asked Questions

Does 2×SEV equal market value in Michigan?

No. In this study, the 2×SEV heuristic did not reliably approximate observed market value.

Using 5,202 closed residential sales from the 2025 GLAR MLS dataset, only 7% of homes sold within ±3% of 2×SEV. Nearly 79% of sales deviated by more than ±10%, and the median absolute error was approximately 19.6%.

While Michigan law defines SEV as approximately 50% of true cash value for tax purposes, this statutory relationship did not translate into consistent alignment with actual sale prices in the market data analyzed. As a result, 2×SEV functioned as an administrative reference, not a reliable valuation proxy.

Can I adjust 2×SEV using taxable value?No defensible adjustment was identified in this analysis.

The study tested whether divergence between SEV and taxable value—often assumed to reflect long-held or capped properties—could predict how far a property would sell from 2×SEV.

Correlation analysis showed no meaningful relationship:

- Total market: correlation effectively zero (R² ≈ 0.00)

- Estate-related subset: weak relationship (R² ≈ 0.08)

Properties with heavily capped taxable values were no more likely to sell near or far from 2×SEV than properties where taxable value closely aligned with SEV. Empirically, taxable value behavior did not provide a usable signal to correct or bound heuristic error.

Why does SEV differ from market value?

SEV differs from market value because it is produced through mass appraisal for taxation, not property-specific market analysis.

Key structural reasons include:

- Assessment lag: SEV reflects conditions as of a prior assessment cycle, not real-time market behavior.

- Property heterogeneity: Mass appraisal cannot fully capture condition, renovations, deferred maintenance, or functional obsolescence.

- Administrative constraints: SEV is designed for consistency and equity across a tax base, not transaction-level precision.

Your findings show that these limitations are not random noise—they systematically prevent SEV from functioning as a reliable proxy for observed sale prices when used outside its intended tax context.

When is it okay to use SEV in probate?

SEV is appropriate in low-exposure, administrative contexts, such as:

- Probate inventory reporting

- Fee calculation

- Procedural filings in uncontested informal probate

In these situations, modest valuation variance has little practical consequence, and Michigan probate procedures explicitly permit the use of assessed values.

However, your data demonstrate that once SEV-based values are relied upon to make decisions—rather than complete administrative tasks—the risk profile changes. The appropriateness of SEV depends not on legality, but on how the value will be used.

In this dataset, 2×SEV did not reliably approximate market value, could not be corrected using taxable value data, and produced materially large errors in most cases—making it suitable for administrative probate reporting, but not for decisions where money, equity, or fiduciary exposure is at stake.

Appendix: Figure 1

| County | Number of Sales | Share of Sample |

|---|---|---|

| Ingham | 2,718 | 52.25% |

| Eaton | 916 | 17.61% |

| Clinton | 651 | 12.51% |

| Shiawassee | 182 | 3.50% |

| Jackson | 147 | 2.83% |

| Ionia | 101 | 1.94% |

| Gratiot | 70 | 1.35% |

| Calhoun | 65 | 1.25% |

| Livingston | 45 | 0.87% |

| Kent | 29 | 0.56% |

| Genesee | 28 | 0.54% |

| Barry | 24 | 0.46% |

| Montcalm | 22 | 0.42% |

| Saginaw | 20 | 0.38% |

| Wayne | 20 | 0.38% |

| Clare | 17 | 0.33% |

| Oakland | 14 | 0.27% |

| Ottawa | 10 | 0.19% |

| Macomb | 9 | 0.17% |

| Kalamazoo | 9 | 0.17% |

| Mecosta | 9 | 0.17% |

| Washtenaw | 9 | 0.17% |

| Roscommon | 9 | 0.17% |

| Lenawee | 8 | 0.15% |

| Hillsdale | 7 | 0.13% |

| Midland | 6 | 0.12% |

| Isabella | 6 | 0.12% |

| Otsego | 6 | 0.12% |

| Mason | 3 | 0.06% |

| Crawford | 3 | 0.06% |

| Cheboygan | 3 | 0.06% |

| Oscoda | 3 | 0.06% |

| Lapeer | 3 | 0.06% |

| Branch | 2 | 0.04% |

| Montmorency | 2 | 0.04% |

| Osceola | 2 | 0.04% |

| St. Clair | 2 | 0.04% |

| Allegan | 2 | 0.04% |

| Gladwin | 2 | 0.04% |

| Monroe | 1 | 0.02% |

| Missaukee | 1 | 0.02% |

| Ogemaw | 1 | 0.02% |

| Manistee | 1 | 0.02% |

| Alcona | 1 | 0.02% |

| Bay | 1 | 0.02% |

| Oceana | 1 | 0.02% |

| Alger | 1 | 0.02% |

| Van Buren | 1 | 0.02% |

| Iosco | 1 | 0.02% |

| Lake | 1 | 0.02% |

| Cass | 1 | 0.02% |

| Benzie | 1 | 0.02% |

| St. Joseph | 1 | 0.02% |

| Grand Traverse | 1 | 0.02% |

| Antrim | 1 | 0.02% |

| Sanilac | 1 | 0.02% |

| Wexford | 1 | 0.02% |

Footnotes

Primary legal references and definitions are cited where relevant; all empirical analysis and conclusions are original to this study.